NAPEO

We are becoming acquainted with disruptions as this year unfolds. A new administration in Washington, a new composition of Congress and sweeping social and technological changes are contributing to a change in the business environment. Disruption comes in many forms, but the most significant for the PEO industry is regulatory change.

In looking back over the years, one of the most significant disruptive periods came when Obamacare was introduced in 2010. Small businesses across America struggled to comply with this new law and the regulatory requirements placed on the workplace. This regulatory disruption opened the door for PEOs to step forward and deal with simple solutions to this complex law. As a result, the ensuing decade saw the PEO industry grow from a fledgling upstart to new levels of maturity.

Next came the pandemic shutdowns and the universal threat that it represented to the population in terms of health and business survival. Once again, the PEO represented the lifeline for small businesses, assisting thousands of small companies in acquiring the critically needed PPP loans.

Now, PEOs have another opportunity due to regulatory disruption – the SECURE Act and SECURE Act 2.0. Some aspects of the laws were effective immediately, but most were phased in over time, especially in January 2025, when auto enrollment became mandatory. The intent of the SECURE Acts is to reach the 56 million Americans working for companies (with 50 or fewer employees) that do not have retirement savings plans. The total working population of the United States is estimated at 172 million. In simplest terms, one-third of all employees in the U.S. have no savings for retirement.

Demographically speaking, this is a rolling economic disaster worsening with each passing year. SECURE Act and SECURE Act 2.0 looked to build upon the proven efficiencies of the multiple employer plan (MEP). PEOs have utilized the MEP since the IRS Revenue Procedure of 2002.

The pooled employer plan (PEP) was introduced as a way for unrelated businesses to aggregate their assets for economy of scale like large corporate plans and MEPs. Along with the economies of scale, also came a new layer of complexity on the already complicated requirements of Employee Retirement Insurance Savings Act (ERISA), which in 1974, established the 401(k) retirement plan for the workplace. The complexity of ERISA is one of the primary reasons why so few small businesses offer a plan to their employees. SECURE Act 2.0 sought to incentivize small businesses to establish a retirement plan by providing a series of tax credits for automatic enrollment, employee count and matching costs borne by the employer. Despite the presence of these incentives, there has been very poor traction among small businesses; once again the complexity of ERISA and now the added complexity of the SECURE Act and SECURE Act 2.0 are a deterrent to making inroads to the 56 million American workers without a retirement savings plan.

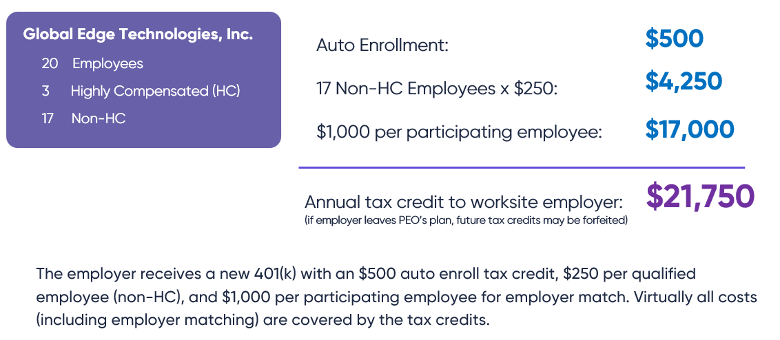

The primary underlying principle is still at work in this environment, the PEO can make the complex simple for small businesses. The PEO is uniquely equipped to handle all workplace related complexities, through the technology of the payroll and HR platforms, but the proven experience of over two decades of HR expertise; hence the 401(k) dilemma facing America is directly in the PEO wheelhouse. For the average PEO client of 20 employees, the total tax credits are just under $22,000 in annual tax credits for up to three years. Here is how it works:

Under SECURE Act 2.0, a new retirement plan for a small business is essentially tax subsidized, creating a virtuous cycle for all concerned.

First, and foremost, the employee receives a payroll-deducted retirement benefit that was not previously available. Because the matching contributions are offset by the tax credit, the employee also receives the benefit of the matching contribution. In many cases, this doubles the contribution for each paycheck.

Second, in a traditional 401(k) set up, brokers, agents and other providers are generally compensated based on plan assets. If there are little to no assets, there is no commission revenue, which can lead to no sale and therefore no plan for a small business. Using the PEOs plan alongside the tax credits available, a small business has access to a 401(k) plan that is both competitive with larger employers and is cost-effective, making it easier for small businesses to attract and retain top talent. Further, the company owner can also participate in the plan and build their own retirement savings as well as his or her employees.

Lastly, the PEO benefits in numerous ways.

- The tax credits lock in a new client for at least three years. If the client company were to leave the PEO, the 401(k) would leave the PEO plan trust and would no longer considered a new plan, therefore, forfeiting the remaining tax credit benefit under SECURE Act 2.0.

- It is proven that the presence of the 401(k) plan substantially increases retention by two-fold in the first two years of the client relationship, and four-fold in subsequent years. The addition to EBITDA is increased materially to the valuation of the PEO.

- Historically the 401(k) has generally been an appendage to the PEO sales process, but now through the tax credit advantage of SECURE Act 2.0, the 401(k) is a leading value proposition to the small business. Not only are tax credits attractive to prospects, but the cost structure of the PEO retirement plan (MEP or PEP) is generally half or less than half or a single employer plan.

THE HORIZON

Last year, while in Washington for NAPEO’s PEO Capitol Summit I had the privilege of hosting a dinner for a dozen members of Congress. Casey Clark, representing the PEO industry, and John Allen of G&A Partners joined me in presenting the effectiveness of the PEO in delivering the 401(k) benefit to small businesses. The PEO is unique in its ability to serve small businesses through its expertise and technology. Nothing in the PEO model is cheap, technology and people are ultimately expensive, and that should be incentivized in the tax structure. I advocated at that dinner that a new additional tax credit was necessary to complete this virtuous cycle – a tax credit directly to the PEO. At the conclusion of the dinner Jason Smith, the Chairman of the Ways and Means Committee stood up and asked the question; “Who is going to write the bill and who is going to sponsor it?” Since then, many more congressmen and women have pledged their support as well as a widening circle of influential organizations. Parenthetically, the NAPEO PAC is a vital voice among Washington policy makers and deserves full support from the membership.

It is my hope that our industry will continue to be the vanguard of small businesses in America. I look forward to the year ahead with increasing momentum to serve shoulder to shoulder with you on behalf of our industry and the vital interests of every small business in America.

-

SHARE

- Copy to clipboard

RELATED ARTICLES

MEET CONGRESSWOMAN ERIN HOUCHIN

Voters in Indiana’s 9th Congressional district elected Congresswoman Erin Houchin to serve in the United States House of Representatives in November 2022. In doing so, Rep. Houchin became the first woman elected to Congress from her district. She also holds the distinction of being the only person elected to Congress who has worked for a PEO.Rep. Houchin spoke to PEO Insider about her decision to seek public office, her experience working for a PEO, and the policies she champions.

BY Chris Chaney

May 2023

NAPEO ADVOCACY DAY IS A HOME RUN

There's an energy around the PEO industry this year that's palpable. Nowhere is that more true than in Washington DC, where we are starting to make our mark as a strong contributor to the vitality and success of the backbone of the economy: small and mid-size businesses. We've got a great story to tell. Help us tell it.

BY THOM STOHLER

August 2023

THINK IT THROUGH: HOW RETURN-TO-OFFICE MANDATES MAY IMPACT EMPLOYEE ENGAGEMENT

As a result of the workforce evolution in recent years, remote, hybrid and onsite work has been redefined, and is a top-of-mind subject in daily conversations. Many companies and teams like ours at LandrumHR have an employee base geographically widespread throughout the U.S. In our case, this pre-dates the pandemic, but like these other companies we, too, are still evaluating the pros and cons to re-engaging teams physically onsite where and when possible, without causing disruption to workflow and requiring facilities (re)construct.

BY Gehan "G" Haridy-Ardanowski

February 2023

STAY INFORMED: RECENT LEGAL DEVELOPMENTS MAY IMPACT EMPLOYERS’ USE OF ARBITRATION IN EMPLOYMENT CLAIMS

Use of arbitration and class-action waiver agreements allows for the private resolution of employment claims on an individual basis. While arbitration is not a low-cost alternative, it can be a very strong hedge against runaway jury awards and swollen class-action damages.

BY STEPHEN CALVERT, ESQ.

May 2023ADVERTISEMENT