NAPEO

CFOs and accounting teams across a wide variety of firms all face a harrowing decision each month – how to accrue for their insurance coverage liabilities. A stable workforce that has a consistent monthly cost makes the problem simple, but variances in types of insurance policies or changes in the underlying exposure base make for a less than trivial exercise. Unfortunately, all these characteristics and more are commonly found in PEOs.

In this article, we’ll talk about how to consider different methods for accruing such liabilities, particularly workers’ compensation. We’ll also share results from a Davies survey of PEO CFOs and finance professionals representing 600,000-700,000 WSEs and how those individuals approach this issue for their respective firms.

WHY ACCRUING FOR WORKERS’ COMP IS NECESSARY

Accurately accruing for retained insurance liabilities isn’t just good practice — it’s a requirement. Unlike other goods or services where revenue and costs typically occur in the same period, there is typically a disconnect between premium and claims costs for insurance liabilities, where claim payments may occur months, years, or even decades after the initial occurrence. As such, GAAP requires accrual accounting to match expenses to the period in which they are incurred, not when cash changes hands. Adhering to GAAP accounting has other benefits, such as:

- Monthly P&Ls aren’t distorted by timing of claims or premiums.

- External stakeholders — lenders, auditors, partners — see a clearer picture of your risk position.

- The company can anticipate and plan for future payouts, both large and small.

While all the respondents to our survey state that they do accrue for WC liabilities, these firms also have been on deductible policies for at least a few years. In our experience through buy-side M&A due diligence, we have seen smaller PEOs newly on deductible plans still using cash accounting.

There are two main approaches to monthly accruals, and one in between.

STRAIGHT LINE

The first approach is the simplest – a straight-line accrual where each month’s accrual is 1/12th of the estimate for the full year.

This approach is ideal for smaller firms that are not seeing material growth, have limited variability in payroll, and/or have fixed premium structures or guaranteed-cost policies.

However, the strength of this approach is also its weakness, as it does not reflect any changes in the underlying exposure base and may result in a larger year-end true-up needed.

VARIABLE METHOD

The second approach is a variable method where the accrual is calculated as a function of different metrics to capture things like seasonality, shifts in business between geographies and industries, starting or ending large projects, etc.

The strength of this approach also lends itself to a weakness. In the complexity of being able to respond to real-time changes, the accrual function itself may need updating over time to ensure that it remains accurate in the future.

It is worth noting that there is a third approach which is a hybrid of straight and variable. For example, one can use a straight-line accruals for 10 or 11 months and true up in the remaining months using the variable approach.

In practice, many PEOs start with straight-line accruals and shift to variable methods as they grow, take on higher-risk clients, and take on more risk through deductibles or self-insured programs.

Noting the profile of most survey respondents being relatively more experienced with deductibles, all respondents stated that they use a variable method. Additionally, roughly 70% of all respondents responded that they “rarely” had a large true-up at year-end while roughly 15% said “sometimes” and the remaining 15% said “often”.

One respondent rightly commented that no accrual method can account for everything, and that there are many things outside of the accrual method that can lead to a large true-up.

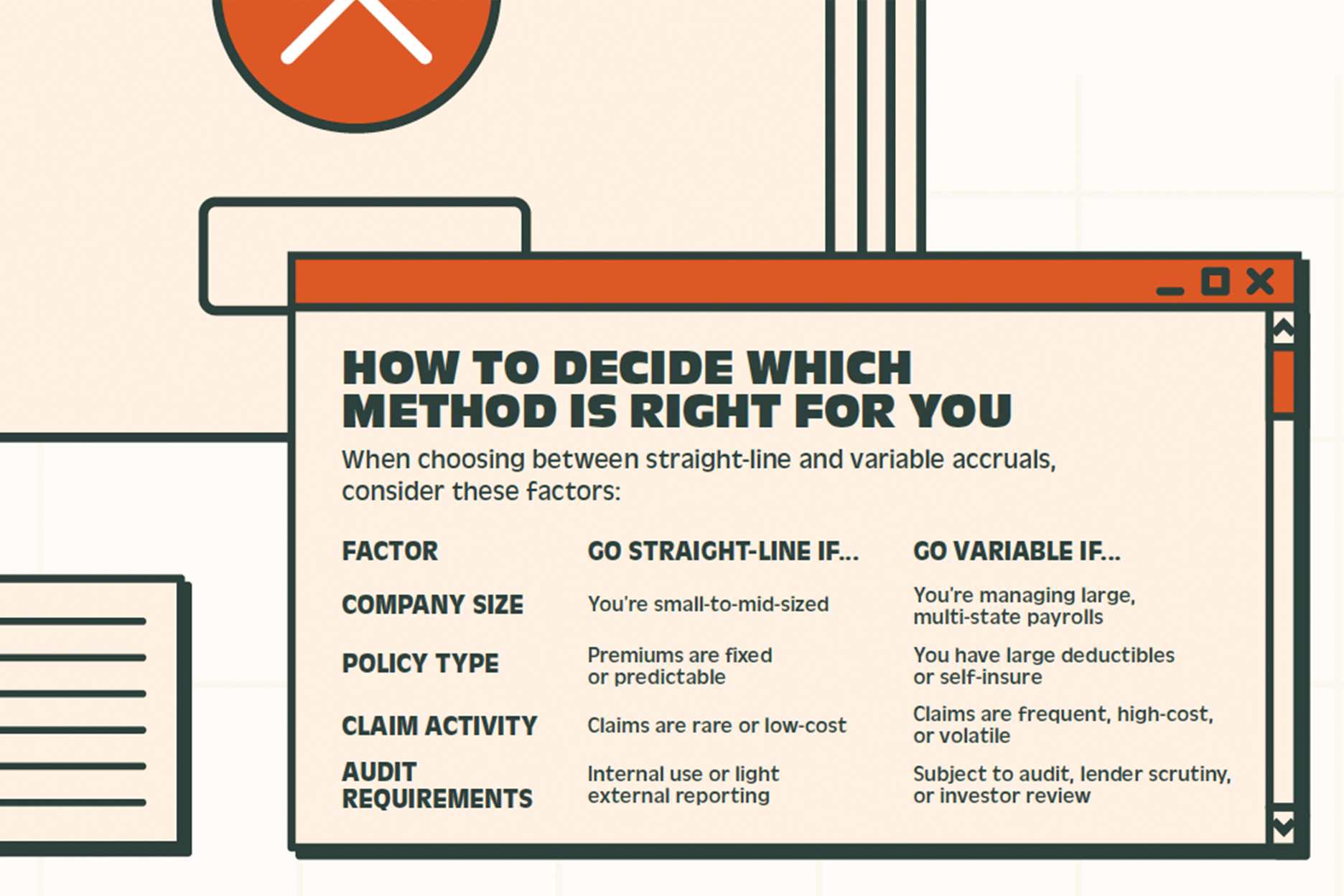

How to Decide Which Method Is Right for You

When choosing between straight-line and variable accruals, consider these factors:

Go Straight-Line If…

- You’re small-to-mid-sized

- Premiums are fixed or predictable

- Claims are rare or low-cost

- Audit requirements limited to internal use or light external reporting

Go Variable If…

- You’re managing large, multi-state payrolls

- You have large deductibles or self-insure

- Claims are frequent, high-cost, or volatile

- Subject to audit, lender scrutiny, or investor review

HEAT CHECK

While a straight-line method might offer simplicity and consistency, a variable approach is often the better approach to capture real-world developments. If you’re considering shifting to a variable accrual model or wanting to confirm that your variable approach is best, consider the following steps.

- Look at whether your aggregate accrual ties to your actuarial report’s point estimate and/or is within the actuarial range.

- Calculate the implied monthly ultimate loss ratio and/or ultimate loss cost for the past 2-3 years and see if the resulting metrics appear reasonable.

- Consider your past true-ups and whether any of those could have been mitigated or prevented entirely through a better accrual model.

If any of the above produce results that appear inconsistent or unreasonable, consider tweaks or wholesale changes to your model. With the right approach, you should have an intuitive and efficient model that will produce accurate and automated monthly accruals.

-

SHARE

- Copy to clipboard

RELATED ARTICLES

CLIENT-LEVEL FINANCIAL ANALYSIS

If you asked someone in the PEO space what he or she thought of actuarial science a positive response might be reserve analyses or accruals. A negative response might be collateral calls or rate increases. Naturally, the varied reactions stem from whether there is positive or negative news coming from the work of the actuary. Yet, one of the most helpful projects an actuary can perform for a PEO, eliciting either positive and negative reactions, is a client-level financial analysis.

BY FRANK HUANG

June/July 2023

PROFITABILITY ABCs: IT IS AS EASY AS 1-2-3

The article provides some simple guidance for streamlining operations (thus reducing selling, general, and administrative (SGA) costs) and increasing gross profit contribution from their existing client base. For the purpose of this article, we are only exploring pricing strategies that affect client profitability and operating efficiency items that impact select SG&A cost categories. Business development and organic growth are excluded from this discussion.

BY Dan McHenry

June/July 2023

THE 5 Ws OF PEO GENERAL LEDGER RECONCILIATIONS

General ledger reconciliation is a key control to help maintain timely and accurate financial statements in any business. If you speak to accounting or finance professionals in the PEO industry, they will agree that general ledger balance sheet reconciliations are the most telling and critical tools in analyzing a PEO’s fiscal position. Failure to reconcile balance sheet accounts timely and accurately can lead to material losses to the PEO. Let’s explore the 5 W’s of PEO ledger reconciliations.

BY JEAN GOLDSTEIN

JUNE/JULY 2023

UTILIZING METRICS AS A PATH TO IMPROVING OPERATIONALLY OVER TIME

A company’s story is often written succinctly on its website, with details of the company’s history, its values, and its aspirations for the future. Internally, however, company leaders can capture a more telling story. Operational metrics, while often unique to each company, depict a different story.

BY Aaron Call

September 2023ADVERTISEMENT